“The biggest risk of all is not taking one.” – Mellody Hobson

DISCLAIMER: The content provided on this blog is for informational and entertainment purposes only. The views expressed are solely those of the author(s) and do not constitute financial advice. Readers should not consider any information on this blog as a substitute for professional financial, investment, or legal advice.

Any actions taken by the reader based on the information provided on this blog are taken at their own risk. The author(s) and/or publisher(s) of this blog will not be held responsible for any losses, damages, or consequences that may arise from following the information, advice, or suggestions mentioned herein.

Please consult with a qualified financial professional before making any financial decisions.

Of all the posts I’ll ever write, this is the one I’m most nervous about writing, because I’ll be talking about how much Anna and I need to retire.

I’m nervous because, until we take our last breath on this planet, we don’t actually know how much money we’ll need. We have no idea what our future will hold nor what our physical and mental health will be. But we have to start somewhere and this post is that somewhere for us.

Anna and I also understand that everyone’s opinions, strategies, and circumstances will be different when it comes to how much is needed and when is the appropriate retirement age. We are also constantly learning new information, updating our strategies, and tweaking past ideas. We would recommend researching different retirement strategies and working with a financial advisor to craft a plan that works for you and your situation. We also encourage you to read the entire post before taking the time to comment.

Before we get much further into the post, I want to define what retirement means to me. I see it as financial freedom to pursue whatever I want in life without the worry of income. Retirement doesn’t mean I’m not working. It just means I can pursue other things in life without having this fear/requirement of needing to generate X dollars each month.

$1.68 million

The short answer is $1.68 million. Thank you so much for reading. I’m glad that is over with :-p :-p :-p.

Okay okay, how did we get to that number?

In the Financial Independence Retire Early (FIRE) community, there is something commonly used called the 4% rule to determine how much is needed to retire early. This is called the FIRE number.

Background

William “Ben” Bengen was a financial planner in the 90s who looked at the stock market history from 1926 to 1976 to determine the safe withdrawal rate of a retirement portfolio. His goal was to find the highest amount that could be withdrawn each year to support a person in retirement for 30 years, with an understanding that the typical life expectancy of a retired person was 30 years. He found a rate of 4.15% could be withdrawn with a portfolio blend of 50% stocks and 50% bonds, but preferred 75% stocks and 25% bonds. The higher stock allocation provided more growth potential compared to the more stable, but lower-interest bonds. He published his study in 1994 and 4.15% was rounded down to 4% because it is a lot easier to say. People have since reproduced the results with more recent data and suggested that 4.5% or 4.8% might be the new safe withdrawal rate. Others have said, Bengen’s initial work was for 30 years and stretching it an additional fifteen to thirty years increases the failure rates. 3.5% would be a safer withdrawal rate.

Side note (just before we hit publish): Bill Bengen recently released an updated study suggesting that 5% may be the new safe withdrawal rate for a 30-year retirement, and 4.15% for a 60-year retirement. His new book, documenting these updated findings, is set to be released on Amazon on August 5, 2025.

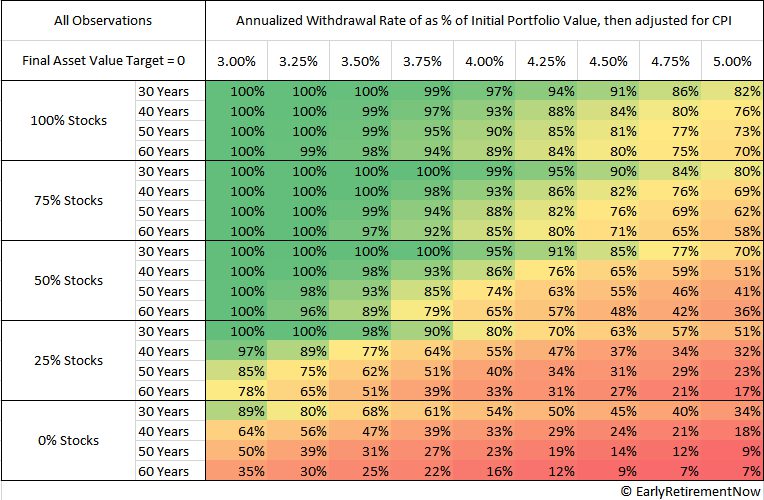

Karsten over at Early Retirement Now has put together an extremely valuable series about how much someone can safely withdraw each year to successfully retire. He analyzed stock market performance from 1871 to 2016 with different portfolio configurations (100% stocks/0% bonds to 0% stocks/100% bonds) from 30 years to 60 years. He came up with over 6.5 million different configurations. His research suggests a 3.5% is the safe withdrawal rate for a 60-year period. Depending on when we retire, we’d be between 105 and 110 years old, but we’d have a success rate of 98%. At 4%, we’d have an 89% success rate.

How much do we think we need

To figure out our number, we have to figure out how much we spend in a year. This requires tracking our spending. It is a scary task because we really have to face our financial demons and guilty pleasures. At the present moment, Anna and I spend between $70k to 75k a year, which includes our mortgage. Our goal is to get our expenses down to $50k, with a paid-off house.

There are four parts that make up a mortgage payment and it is abbreviated as PITI:

- Principal – Amount owed on the house/loan

- Interest – The cost to borrow that money

- Taxes – Money paid to the state for owning a house

- Insurance – Amount to protect the house in case of some kind of damage

We forecast we’ll have the house paid off in the next two years. We currently spend $12.7k a year on the principal and interest, which will bring our current expenses down to $57.3k to $62.3k. We still have a bit of trimming to do, but we are getting there. There will be a whole series of posts later about how we are cutting down our expenses.

The reason why we are paying our house off early vs investing that money is a topic for a separate day. Right now, we are putting it in a high-interest savings account, that is earning more interest than our loan. We’ll then pay the house off when we’ve accumulated enough money. In the meantime, this is acting as a secondary emergency fund.

Life Protection Strategy #1 – Withdraw Cushion

Assuming a perfect scenario, we’d need $1.43m ($1.43m*3.5% = $50,050). But, we know life isn’t perfect and things can happen, so we are rounding that up to $1.5m. That would make our withdrawal 3.3% ($50,500/$1,500,000). Or give us an extra $2,500 a year ($1.5m*3.5%).

We have also discussed the idea of increasing our number to $1.7m which would give us $59,500/year ($1.7m*3.5%) to give us a bigger cushion per year. Alternatively, the likelihood of us living to 110 is pretty low. Maybe a 3.75% withdrawal rate for 50 years would be better. That would give us $56,200/year ($1.5m*3.75%) or $63,750/year if we increased our number to $1.7m at 3.75%. Decisions decisions. We have several more life protection strategies we’ll be talking about in this post if we did need more money.

This $1.5m isn’t just sitting underneath our mattress in our soon-to-be paid-off house. It is invested in the stock market between index funds, 401k, and ROTH IRA. We are choosing a 100% stock allocation for our portfolio to provide the highest level of success.

In the stock market, you can buy a single share of a single company. For example, one share of Apple. This could be risky if Apple goes down or could be positive if Apple goes up. A way to spread out that risk is by buying shares of multiple companies. This could be done individually, or it could be done by buying a collection of companies. A well-known grouping of companies is called the S&P 500. These are the top 500 companies in the US stock market.

Each brokerage (a place where we can buy and sell stocks, bonds, and other investments) has its own collection of companies called indexes. Two popular index funds from Vanguard are VOO, mirroring the S&P 500, and VTI which are all the companies in the US stock market. If you buy one share of VOO, you are buying a tiny piece of 500 different companies. This spreads the risk out and ensures if one company’s share price goes down, it doesn’t massively impact your total stock portfolio. With each paycheck, we invest in five different index funds:

- VOO – Mirrors the S&P 500

- VTI – All the stocks in the US stock market

- VXUS – International index of companies in developing and emerging countries

- ONEQ – Mirrors the NASDAQ (National Association of Securities Dealers Automated Quotations). Primarily focuses on technology stocks, but also includes healthcare, financial, retail, food, and entertainment. Includes mostly US companies, but also some foreign companies.

- DHS (WisdonTree U.S. High Dividend Fund) – Not the package delivery company, but several companies with a high dividend amount paid out per share. More to come on this index in this post.

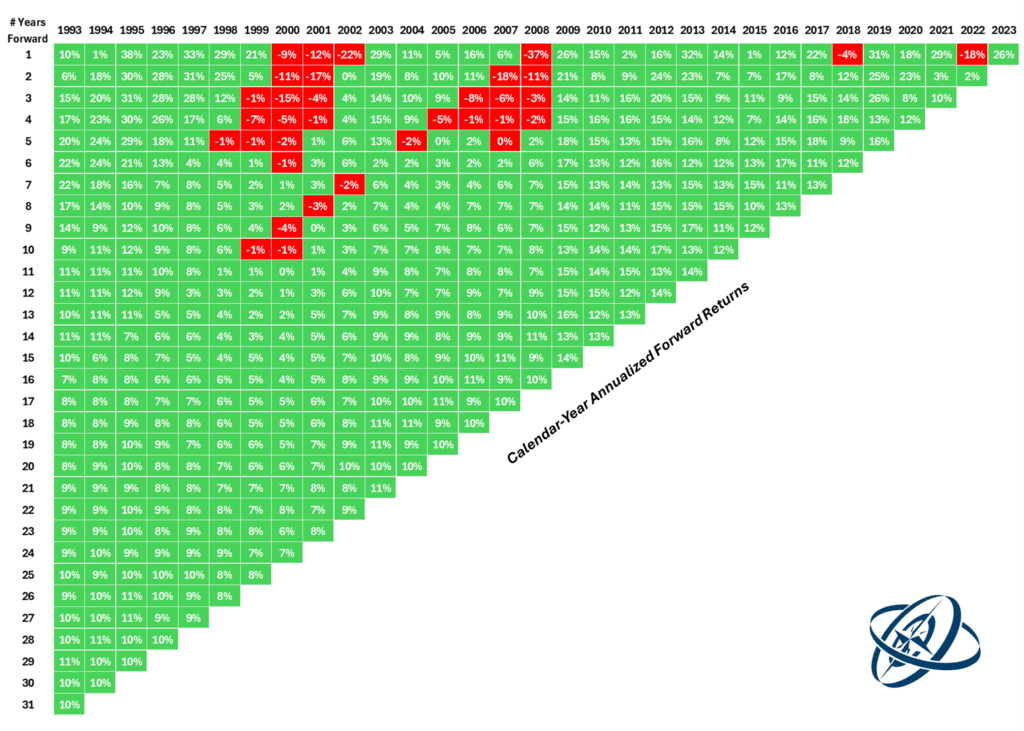

If you look over the history of the S&P 500, it has rarely lost money. Ben Carlson over at A Wealth of Common Sense looked at thirty-one years of the S&P 500 returns from 1993 to 2023 and found the average growth was 10%.

Inflation

The next piece of information we need to talk about is inflation. Inflation is how much an item/service goes up in price each year compared to last year. On average, the price of everything goes up by 4% per year. Side note, if your money is sitting in a checking/savings account and earning less than 4%, it is becoming less and less valuable over time.

Year 1: $50,000

Year 2: $52,000 ($50,000 x 4%)

Year 3: $54,080 ($52,000 x 4%)

Luckily, we have our $1.5m invested in index funds that return 8 to 12% each year and the extra money is reinvested along with the dividends. That means, in a perfect scenario, it would take a very long time to run out of money. In fact, we should have more money than we started with when we take our last breath. But, we know the world isn’t perfect. Because we are pulling out less than we are earning on average/selling fewer shares, in the bad years we can access that extra money/sell additional shares that we don’t need in the good years.

The other assumption is, we actually need the extra money to compensate for inflation. Just because inflation goes up, doesn’t necessarily mean we have to take the extra money out. For example, if someone has a mortgage, the principal and interest amount doesn’t also increase by 4% each year. The taxes might, but that is a smaller amount when compared to the principal and interest. In our case, are we able to figure out how to reduce our expenses?

Life Protection Strategy #2 – Extra Income

Just because I’m retired, doesn’t mean we won’t be generating income. Anna works as a fitness instructor. For the time being she wants to continue working because it brings her joy. Any classes she teaches offset the amount of money we need to withdraw from our stock portfolio.

Anna and I have several other sources of income:

- Anna’s photo store

- Affiliate marketing

- Website

- YouTube

- Anna D and Adam (Travel Adventures)

- Go2Spin Fitness (Anna’s Cycle Channel)

- Stock video royalties (Selling video clips for people to use in their videos)

- Sponsorships for our YouTube channels

All of these offset the money we need from our stock portfolio. Each year, we take on new projects/goals to generate new income and my plan in “retirement” is to continue growing them and adding new ones. The biggest threat to the 4% rule, or 3.5% rule in our case, happens in the first five to ten years. Any massive changes (life events, stock market crash, unexpected cash needs) have the biggest impact on the amount of money generated over time. If we continue for even just a few more years of generating extra income, we drastically increase the overall success of our early retirement plan.

Life Protection Strategy #3 – Emergency Fund

You might be thinking, stock markets crash, what about your money then? In the US, the average “stock market crash” or recession lasts for 18 months. Most are less than 12 months, but the dot com bubble and the Great Depression are the longest. The dot com bubble took 15 years for the NASDAQ to fully recover. Below are a few notable examples:

- 1929 – Great Depression – 42 months

- 1937 – Recession – 13 months

- 1945 – Recession – 8 months

- 1949 – Recession – 11 months

- 1953 – Recession – 10 months

- 1958 – Recession – 8 months

- 1960 – Recession – 10 months

- 1969 – Recession – 11 months

- 1973 – Recession – 16 months

- 1980 – Recession – 6 months

- 1981 – Recession – 8 months

- 1987 – Black Monday – 2 days

- 1990 – Recession – 8 months

- 2000 – Dot Com Bubble Burst – 180 months

- 2001 – Recession – 8 months

- 2008 – Housing Crisis – 18 months

- 2020 – Coronavirus – 2 months. Side note, the S%P 500 had an 18% return in 2020.

This is where our two next life protection strategies come into play and how we get to the $1.68m I mentioned earlier.

If you had a chance to read the post on Getting Out of Debt, we talked about Dave Ramsey’s baby steps. These helped Anna and myself get out of $35k in debt. Two of the baby steps are setting aside an emergency fund. Anna and I have $60k in a high-interest savings account, in case we need the extra little bit, which is earning more than 4% in interest each year. This gives us a full year of extra protection in fast and easy cash. At least while we’ve been working, we’ve been increasing this number by 4% each year to keep pace with inflation, in addition to the interest we’ve been earning.

Life Protection Strategy #4 – CD Ladder

For our second stock market mitigation strategy, Anna and I plan to have a two-year CD Ladder (Certificate of Deposit Ladder). A bank or credit union will offer CDs or the US government will offer bonds. A bank or the government says, hey, loan us some money and we’ll pay you back plus interest in X days/months/years.

For example, we can buy a $10k bond from the government for ten years at 4.2% yield per year. At the end of ten years, our investment would be worth $14,859.47 and the government would give us a check, minus taxes on the $4,859.47 of course…

Rounding up to $60k again, if I plan to retire in 2029,

- Q1 2027 buy $15k worth of bonds/CDs for a 2 year period

- Q2 2027 buy $15k worth of bonds/CDs for a 2 year period

- Q3 2027 buy $15k worth of bonds/CDs for a 2 year period

- Q4 2027 buy $15k worth of bonds/CDs for a 2 year period

- Q1 2028 buy $15k worth of bonds/CDs for a 2 year period

- Q2 2028 buy $15k worth of bonds/CDs for a 2 year period

- Q3 2028 buy $15k worth of bonds/CDs for a 2 year period

- Q4 2028 buy $15k worth of bonds/CDs for a 2 year period

The day I retire, we’d have $120k invested in bonds/CDs. That is two years of living expenses, plus some extra, in a very stable investment, unless the US government goes bankrupt or the bank crashes that we bought the CD from.

In Q1 2029, $15k plus interest would be returned to Anna and myself. If we don’t need the money, then back in a two-year CD/bond it goes. In the event of a stock market crash, we could either live off our emergency fund, the money from the CD/bond, or a mix-and-match. With the average stock market crash being 18 months, this allows us to not touch our portfolio while we let it come back to pre-crash numbers and allows for continued growth.

In the years leading up to the crash, we are withdrawing less from our index funds than we are making, which also enhances our cash cushion.

This is how we arrive at $1.68m ($1.5m + $120k + $60k).

Life Protection Strategy #5 – Yield Shield

We first heard of this term from Kristy and Bryce at Millennial Revolution. In regards to the stock market, yield is the amount of money paid to investors. These are dividends paid by a company to investors at the end of the month, quarter, or year. Anna and I have strategically picked a mix of funds. Most are higher growth, but DHS is dividend-focused.

- VOO – 1.21%

- VTI – 1.21%

- VXUS – 0%

- ONEQ – 0.60%

- DHS – 3.46%

The dividend payouts are where the yield shield comes into play. By default, we are reinvesting any money we receive back into our stocks to grow. But, during a period when the stock market is down, we can instead turn that behavior off and have the money deposited into our account. That gives us another source of income, in a worst-case scenario. For example, if we plan to have 20% of our portfolio in DHS ($1.5m * 20% = $300k). During a stock market crash, we could turn off the reinvesting behavior and receive $10,380 in dividends ($300k * 3.46%) over the course of the year (they pay out monthly). It doesn’t give us the full $50k, but provides some pressure relief. Plus, we could do that with VOO and VTI with their 1.21% yields.

A risk with this strategy is, will companies also reduce the amount of dividends they are paying out each month/quarter/year? It isn’t a guarantee.

A second risk is, the stock market is down. So are the share prices. By not reinvesting the dividends, we are not buying shares at lower prices. This could hurt us later on because the long-term growth is being stunted.

This is an absolutely worst-case situation.

Note: The dividend amounts shown above are likely to fluctuate and may not be the same when you read this post.

Life Protection Strategy #6 – Flexibility/One More Year

The goal is to retire in five years. But that isn’t a requirement. If things in five years aren’t looking great (stock market decline, higher annual budget, or some other kind of expense), we can continue working. We can delay it by a few years. Even if I retire at the age of 55, it will still be ten years earlier than the average male in the US.

This flexibility also allows us to avoid something called the sequence-of-returns risk. If we retire when the stock market is down, we’ll need to sell off more shares to get to the $50k amount than when the stock market is doing well. For example, if we have 5,000 shares of a made-up index fund and the price per share drops to $25. Then we’ll need to sell 2,000 of our shares to withdraw $50k ($50k/$25). Five, ten, twenty years down the road, there would be a greater impact than if the share price was $100 a share. In that situation, we’d work a little longer to ride out the downturn of the market and continue investing.

Life Protection Strategy #7 – Geographical Arbitrage

Lastly, there isn’t a requirement to live in the US. It would be ideal, but not a requirement. We could move to a lower-cost country and rent our house out. This would be an absolute last resort, instead of getting a job to make some additional income. With a paid-off mortgage and a house emergency fund of $25k, we’d bring in an additional $1,365 monthly. We pre-allocated the emergency fund because if we ever got to that point, we are in serious money trouble versus deducting a percentage each month to set aside for emergencies/vacancies/maintenance. As money would be used from the emergency fund, then we’d set aside a percentage from the rent to replenish it.

Kristy and Bryce at Millennial Revolution have a quote, “When sh*t hits the fan, we’re moving to Thailand.” I think it sums up this point. They also wrote a book called Quit Like a Millionaire that was really helpful in teaching us the concepts of how to retire early.

Life Protection Strategy #8 – Social Security

Up to this point, I haven’t mentioned anything about Social Security. Social Security isn’t factored into our calculations, but it will be something we have to start taking at some point. The minimum age is 62 and the maximum age is 70. Our current plan is for Anna to start collecting at 62 and for me to wait until 70 to collect the maximum amount. This will provide an extra cash source. I could collect early if there were a need.

Fears

So that is our retirement plan, and it terrifies me. There are so many unknown factors that could completely blow up the entire plan. Three items that come to mind are health, cars, and houses.

Health, we don’t know what is going to happen with our bodies and minds as we age. Are we going to need procedures, surgeries, or other care that we can’t predict?

For cars, my daily driver is 22 years old, and Anna’s daily driver is 16 years old. It is getting harder and harder to find parts as things break. At some point, we might be forced to buy a new car because we just can’t find the parts we need to fix something. According to Kelley Blue Book, the average price of a car is $49,740 in 2025. That would be the equivalent of an entire year’s worth of our lives that we would need to budget for.

Without going into a full story, this actually happened to Fez (2018 Subaru Forester). The airbag sensor went bad. If there was an accident, the airbags on the passenger side would not be triggered. We took it to Subaru and they said they wouldn’t have a replacement part available for six to nine months at the earliest… They had several customer cars sitting in the sun, on top of a parking deck, rotting away for over a year already waiting for the part to come in… After five months of waiting, no update on when they would manufacture the part, and several more cars showing up for the part, we wound up buying a new car…

Lastly houses. We’re talking about paying this house off within the next two years. But is this our forever home? Buying a new house could be extremely expensive, plus we would no longer have traditional W2 income. Could we get a mortgage?

References

https://www.fool.com/investing/stock-market/basics/crashes

https://www.investopedia.com/terms/d/dotcom-bubble.asp

https://www.treasurydirect.gov/BC/SBCPrice

https://kyestates.com/wp-content/uploads/2015/02/Bengen1.pdf